Are you giving your kids or teenagers a financial literacy class or do you expect the schools to take care of that objective? Last week I went to the info evenings of the schools of our sons. No financial literacy classes during the whole school year 2018 – 2019….NONE !! So the school educational system is failing….no doubt.

That is one of the reasons why we started our blog as we see too many people around us with poor financial literacy skills. We can’t afford that the school system fails our kids. We can’t let them enter the real life without knowing how to grow their money and just continue to put their money on a savings account. We have a responsibility as a parent.

In January 2018, we did set our Financial Education objectives for the year. You can read them all in our blogpost “2018 Financial and Travel Goals“. We did one financial education practice class in 2018 where one son was allowed to travel to London on a fixed budget. That was a very interesting journey !

Politicians are NO example for financial literacy

In the financial Newspaper De Tijd one of my favorite sections is always “the 10 Money Questions to…”. A politician, a businessman, a musician, ..someone known in Belgium gets asked 10 money questions. The most interesting question for me is always how do they teach their kids financial literacy or how do they invest their money ?

Past week the politician Ms. Liesbeth Homans was being questioned. She gave two shocking answers according to me. The financial education she gave her son was to show all her expenses to emphasize the need for education and pay the bills later in life. A smart move to show him the bills but that doesn’t mean her son can manage a budget later in life, right? I assume that is where her financial education stops…

Past week the politician Ms. Liesbeth Homans was being questioned. She gave two shocking answers according to me. The financial education she gave her son was to show all her expenses to emphasize the need for education and pay the bills later in life. A smart move to show him the bills but that doesn’t mean her son can manage a budget later in life, right? I assume that is where her financial education stops…

The second shocking answer was the answer on how this minister in the Flemish government invests her money. She simply puts everything on a regular or savings account. Wow ! Has she ever heard of the impact of inflation ? She isn’t allowed to invest in the stock market (which is probably a segregation of duties law from the dinosaurs time) but I am sure there are ways to solve that. A colleague minister in the Flemish government was invested in different companies. What shocks me is the fact that a politician is putting all her money on a savings account…as an emergency buffer she says. I have written numerous blog posts about the emergency fund. Here’s the latest blog post about our strategy.

Our Emergency Fund Strategy : Benchmarking and Execution

I think this blog post will be very useful for Ms. Liesbeth Homans. I can’t blame her lack of financial literacy as this phenomenon in Belgium is a vicious circle. The school system fails, the parents don’t get educated,..so how can the kids get educated ?

Financial Education Class 5 : Inflation

Sunday evening past week was a perfect evening for another financial literacy class. The great thing is that they are getting more and more excited about these classes…it’s all about money !

Inflation is not an easy topic to explain but I keep it as simple as possible. Please find below the description of the different slides of the presentation. You can download the Dutch and English presentation including the exam questions in a Word document in the Our Presentations Section below. Use it to teach your kids !

Inflation is not an easy topic to explain but I keep it as simple as possible. Please find below the description of the different slides of the presentation. You can download the Dutch and English presentation including the exam questions in a Word document in the Our Presentations Section below. Use it to teach your kids !

Here you find the explanation of each slide and what the key message is while giving this financial education class to your kids. You will also find this in the Notes Section of each slide. Read below the section of what my students think about this class.

Slide 1 : Inflation – Losing money without realizing it !

The goal of today’s financial class is to learn about the inflation and how it impacts your financial life. This topic “inflation” will impact your whole life. Why ? Because it has an impact on your savings, your expenses,…everything. So it is very important you understand what inflation means and how you should act going forward…got it?

Slide 2 : What did you learn last time ?

First of all let’s see what you still remember from previous financial education classes? Let us check if you remember what you learned during Budget Fun, The Compound Interest and Financial Pyramid class. Go to your Exam page and fill in the first three questions on page 1.

Slide 3 : Exercise 2 : Let’s repeat Compound Interest

Let us repeat an exercise how to calculate the compound interest. You get 10.000$ and you want to grow your money with 7% per year. How much will you have at the end of year 10? Can you calculate me the correct amount?

Did you know that the majority of young people do NOT know the principle of compound interest? It is one of the most important financial concepts to understand!

Time to write down your answers to questions 1 and 2.

To my pleasant surprise, they both complete correctly the compound interest table and write down the right answers to the question “Why is a budget important?”. We discuss jointly the different answers that they wrote down.

Slide 4 : Answer to exercise 2

Let’s check your answer and let’s see if you calculated correctly. Give me some conclusions from your calculations.

Be aware that as the amount of years increases, the amount grows exponential and you get a snowball effect where the amount grows exponentially.

Slide 5 : Key Principles of Compound Interest

Let’s repeat the three key principles of compound interest. The first one is the annual rate of return or growth rate of your money. How fast can you grow your money ? The second one is TIME. You need to let time do its work and grow it over time. The third and also important factor is your additions to your total amount per year. You can see the effect on the graph. Over time the amount compounded grows exponentially…do you understand this?

Slide 6 : Do you remember your Financial Pyramid?

Name the four pillars of the financial pyramid. This is the question 3 on your paper. Do you remember?

Slide 7 : Your Financial Pyramid

Let’s review your answers. I am very happy that they remember. I explain the meaning and importance of each layer in the financial pyramid. Go to Financial Education Class 3 if you want the full explanation.

Slide 8 : Why Financial Education is important…

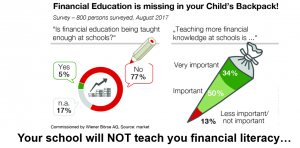

Why is financial literacy important? I explain the kids that financial education is simply missing in their weekly schedule. They get both two hours of religion per week. How will religion serve them in their future life ? More than financial literacy? Kids do agree with me !

The numbers in this graph are clear that financial education is NOT taught at schools while it is extremely important!

Slide 9 : Topic of today’s class : Inflation

Today’s lesson is about how inflation works and what it does mean. You will be impacted by inflation your whole life ! Governments like inflation. Look at the little guy on the top left. Inflation is a heavy ball around his leg. It is like a hidden shark in the water or a lady losing her shopping goods over time…three great cartoons that represent inflation.

Slide 10 : How banks work with your money

Let’s begin with explaining how banks operate with your money. You put the money you get from grandmother in a savings account. The bank will pay you minimum 0,11% on the money you park there. They take that money and give it someone else who want to take a loan to buy a house, a car, a vacation, start a company at 3%. A government also takes loans with central banks. The ratio from savings towards loans is around 1:10. They can give a % money to 10 people for every person putting money on the bank.

So I ask the kids…is the bank earning money ? They figure it out quickly.

Slide 11 : Debt is still money

So if you take a loan at the bank as many Americans do for their house, car or study at university, they need to pay that money back. Debt is still money. It is just a matter of how long will it take before you pay it back.

Slide 12 : Interest Rate

So each loan has an interest rate. Interest rates are defined by central banks and commercial banks. The higher the interest rate goes, the more you have to pay if you have a variable interest rate. If you have a fixed interest rate, you have a fixed amount to pay. Most Belgians buy a house with a fixed interest rate loan.

Past years this interest rate has been going down. Now it’s going up a little again.

Slide 13 : The definition of inflation

Read the definition of inflation. Do you understand this ? It is when prices of goods and services are constantly going up. You don’t know about this as today you pay 1 euro but tomorrow you pay 1,15 euro. Small increases of prices over time. Do you understand ? Not really…so let’s explain more in detail.

Slide 14 : Why should I care Brother ?

So why should you care ? Well inflation means that if prices goes up, your expenses will increase. For example, if you rent a house and your contract says “Rent will be adjusted according to inflation rate”, that you will pay more each year to a new adjusted inflation rate monthly fee. Got it?

Slide 15 : Losing Buying Power

Let’s take a look at the left image. What do you see ? You can see the shopping basket of the year 1998, 2005 and 2013. What do you see ? How much can you buy for 20 dollars ?

Inflation is robbing you slowly from your purchasing power. Do you see the difference ? When prices go up, your purchasing power goes down as time goes on.

This is very important to understand !

Slide 16: The evolution of the price of one bread

Here you see the graph of the price of bread. What was the price in the year 1990 ? What was the price in the year 2010 ? What will be the price of bread in 2030? We don’t know but you understand now what is happening, right ?

Slide 17: Inflation, the hidden tax

So inflation is actually a hidden tax we pay for living in this world. The prices go up each year and governments also want inflation to go up. So if you don’t grow your money higher than inflation, you are losing money.

Do you remember how much interest the bank gives you on your savings account ? Right…o,11%

Slide 18 : What is the % Inflation today in Belgium ?

Let’s read the following graph. Can you tell me the inflation rate in Belgium in July 2018 ? What is the % ?

So this means 2,17% was the increase in price if your rental contract stated that each July your rental fee will be adjusted according to the inflation rate. Understand ?

Slide 19 : What is the impact on your Savings Account ?

So let’s do exercise on the next page. Calculate how much money or buying power you have left after 10 years of an inflation of 2%. It is the same concept of compound interest but now you are losing money.

The answer is : around 8.000. After 10 years you will have lost almost 20% of your buying power. It will still show 10.000 on your bank account but you only have buying power of 8.000 Euro.

Slide 20 : In Venezuela They have Hyperinflation

So there’s also HYPER inflation. What does that mean ? It means the prices go up exponentially and money is worth almost nothing. Here you see a pile of money on one side versus a roll of toilet paper. Well…the money is worth less than the toilet paper so it’s cheaper to clean your butt with the toilet paper…lol !

If your country will do a hyperinflation, run and move to another country. You are in a bad spot !

Slide 21 : Let’s find out your financial attitude

Managing money is also about your financial attitude. Let’s flip to the next page. Take a look at following money options. Which one would you choose? Write down why you don’t want to chose an option and mark which one you would chose?

When the kids are ready, they explain their reasoning.

Son A choses for the 1 million $ cash. This gives financial security. He doesn’t think spending time with a rich person provides any value nor money. Lifetime free traveling is nice but not important. No risks for winning the 200 million as you could end up with nothing.

So conclusion of the financial attitude of son A : Risk averse and aiming for financial security. Take the money opportunity and grow your money from there. Son I choses the 50% chance at winning the 200 million. His reasoning is that he has nothing today, so if he has nothing afterwards..nothing changes. If he wins it, he is financially independent and doesn’t need to work anymore. Even his family doesn’t need to work anymore. The other choices are not appealing to him.

Conclusion of the financial attitude I : Doesn’t shy money risks, nor a gamble. Taking the 1 million cash is not sufficient for him…it’s not that much money according to him. What do you have left after buying a house and more stuff ? This leads to an interesting discussion and lot of laughter. I explain the kids spending three years with the richest person on earth can teach you how to grow your money, how he made his success and how he can help you to build your own business by mentoring and coaching you. Lifetime free traveling can also teach you many valuable lessons in life. You learn how to deal with travel problems, learn about other cultures and interact with foreign people.

Slide 22 : Final feedback

Time for final feedback. Kids write down their final feedback and what they did learn. We end with a present.

Slide 23 : Keep on learning EVERY DAY

Never stop learning as this is important in life. Follow your passions and learn, learn, learn…

Feedback and Key Learnings from my students

Getting teenagers engaged for a financial education class may be challenging. When I ask other parents what they do for their kids related to financial education, I get answers like “why (should I)?” or “how” or “my kid is not interested”.

What was their feedback and three key learnings from this class ?

- We learned that inflation can effect so much your life and hyperinflation can make you lose your money

- We learned what banks do with our money…

- When you chose a savings account, make sure you chose a bank that has a FREE regular account. Otherwise you pay more money in one year than you get money from your savings.

Our presentations

Download here our training material

English version :

DividendCake_Kids Financial education 2018 Class 5 FINAL

Blog post Kids Financial Education 2018 Class 2 Questionnaire

Dutch version :

DividendCake_Kids Financial education 2018 Class 5 Dutch

Blog post Kids Financial Education 2018 Class 2 Vragenlijst

Final Words

So the financial education class 5 has been posted. Now it’s up to you as a parent to teach your kids…you have a responsibility. What was the present we gave our kids as an incentive for attending this class. we gave them a book.

It’s the book ” How to turn 100$ in 1.000.000 $” by

So this was the end of our class…do you want your kids to learn financial literacy ? Stop your excuses, educate yourself and teach your kids so they are prepared for the real life.

With our blog, we can have an impact in educating financial literacy and helping parents ! You can download all our training materials for free. We hope you appreciate our effort and many hours putting this together.

Leave a comment if you like what we are doing. Thanks for following us on Twitter and Facebook and reading this blog post.

As usual we end with a final quote.

No Comment

You can post first response comment.