Recently I read on the blog website of ThePoorSwiss his reflection on “Emergency Fund – Do you really need one ?“. As a married couple, he has build up an emergency fund of around 13.000 Euro. His strategy is to reduce this emergency fund going forward. In the FIRE bloggers community there is lot of debate of the need for an emergency fund. Big ERN at earlyretirement has an emergency fund of 0$ and gives you 10 reasons why they are not are good.

Since the start of this blog, I have written several blog posts about our emergency fund. The latest one was how to correctly size your emergency fund.

Do you correctly size your Emergency Fund?

Sizing your emergency fund is probably the biggest topic of discussion for households. 15 % said they prefer to enjoy life and spend money. Today we reflect on how we benchmark our financial savings buffer, the layer 1 in our Financial Strategy and explain you how we fight inflation for our financial buffer.

Benchmarking against America’s households

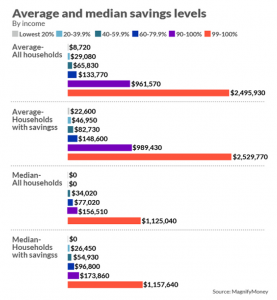

While being in Corporate America the past week, we bumped upon the article “Brace yourself, this is how much America’s 1% has saved” of Quentin Fottrell at the website MarketWatch.com. In this article we learn that the median American household currently holds just $11,700 in savings, according to a new analysis of Federal Reserve and Federal Deposit Insurance Corp. data by personal-finance site Magnify Money. The top 1% of households in the U.S. by income have a median savings of $1.1 million across a variety of saving accounts. The bottom 20% by income have no savings accounts and the second lowest 20% income earners have just $26,450 saved.

Stagnant wages, student debt, soaring house prices and rising credit-card debt have not helped people save. Each time when I go to the USA, I notice that life becomes more expensive and salaries have not gone up much during past years. “Lots of families are living paycheck to paycheck and struggling to save even a little,” said Caroline Ratcliffe, a senior fellow at the Urban Institute, a nonprofit policy group based in Washington, D.C. “Limited savings isn’t only an issue for low-income families. Quite a few middle- and high-income families have no savings cushion to fall back on. One in 5 middle-income families and 1 in 10 high-income families have no retirement savings.”

“Low-income people can save,” Ratcliffe said. The most common advice is to start saving early and often to benefit from compound interest, which adds interest to both the capital and the interest already earned.

Very few of the 126 million U.S. households covered in the latest data are average. “As of 2016, about 78% of households had at least one of the following: a savings account, a retirement savings account, a money market deposit account or certificates of deposit,” it said. The bad news: Just over half of Americans own stocks, a Gallup report recently concluded. That includes 401(k) plans, shares in an equity mutual fund and/or an IRA account. Two-thirds of Americans do not even participate in or have access to a 401(k) plan, according to the U.S. Census Bureau.

There is also wide disparity in saving, based on age and income, and whether you look at the average or median (midpoint), MagnifyMoney added. Millennial households have an average $24,190 in savings, but half of millennials has less than $2,430 saved. Generation X households have an average $125,560 saved, but half has less than $15,780 in savings, checking or retirement accounts. Baby boomers and older have an average $274,910 saved, but again half that cohort has less than $24,280 saved.

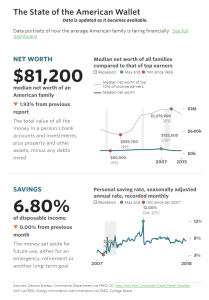

The poorest Americans fare the worst. Some 50.8 million households or 43% of households can’t afford a basic monthly budget for housing, food, transportation, child care, health care and a monthly smartphone bill, according to an analysis of U.S. government data released earlier this year by the United Way Alice Project, a nonprofit based in Cedar Knolls, N.J. “For too long, the magnitude of financial instability in this country has been understated,” said John Franklin, chief executive of the United Way Alice Project. In 2017, 44% of people in the U.S. said they could not cover an unexpected $400 emergency expense or would rely on borrowing or selling something to do so, down from 46% the year before, according to a separate report released last year by the U.S. Federal Reserve.

When we benchmark our Emergency Fund against the average and median savings levels, we are in the 50% range by income of American households. Today our emergency fund totals 46.500$. That amount equals the 40% average households with savings. When we compare with the median saving, our emergency fund is above the 60% of median savings for all households. When comparing with median households with savings, our emergency fund equals around 40%. When you look at the total net worth of the American Wallet (81.200$), our emergency fund equals more than 50% of the median net worth of all families. Please note that the value of our dividend portfolio is not included in our benchmark with the American savings. We only use the total value of our emergency fund.

Our Emergency Fund Strategy

Keeping money in a savings account, makes you poorer each month and each year thanks to the inflation rate. In the inflation rate graph, you can see the inflation rate in Belgium for the past 10 years. The inflation rate has been ranging between 0 and 4%. Since 2015 we have the inflation rate go back up to 2,17% in July 2018.

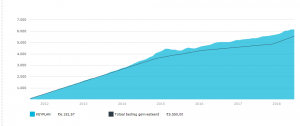

In 2011 the total of our emergency fund was 55.000$. In 2012 as interest rates were going down on our emergency savings account, I decided to decrease the total amount on our savings account. And I decided to start a fund investment plan to compensate the inflation rate of our savings account.

During the past 6 years we invested on average 65 Euro per month in this Unexpected Costs investment plan. Since 2018 we increased this amount to 100 Euro per month. The total invested money Year-to-Date is 5.550 Euro and the current value is 6.152,57 Euro. (or 7150 USD) That is a net gain of 602,57 Euro. That is 10,8% return on our invested money.

Looking back at our decision of 2012, we can conclude it was the right decision to offset the inflation increase over past years and the decrease in interest rates on our savings account of our emergency fund. We will continue to invest on a monthly basis in this investment plan and keep our emergency fund flat with no additions of new cash.

Final Words

Going forward, we will evaluate the size of our emergency fund each year. Today 18% of our emergency fund “Unexpected costs” sits in an investment plan and 82% in a ready available savings account. Dependent on interest rates and the direction of the stock market, we can always adjust the proportion between both. The good thing is that I can always take money out for a big expense going forward. I don’t feel bad about having less money in our emergency fund today compared to 2011. The money I took out of our savings account in 2011 allowed me to start my dividend investing strategy and build the portfolio that gives me today 500$ average per month. Do what you feel is right for your family.

It was interesting for us to reflect on the size of our emergency fund and see how it compared to American households savings. You can do the same today. How does your emergency fund and savings compare to above stats ? Well, we hope you learned something from this blogpost and how we think about an emergency fund strategy.

Don’t hesitate to leave your comments and feedback. Let us know what you think.

Good luck with your personal finance strategy! Thanks for following us on Twitter and Facebook and reading this blog post. As always we end with a quote.

No Comment

You can post first response comment.