Are you giving your kids or teenagers a financial literacy class or do you expect the schools to take care of that objective? Maybe you need a financial education class as a parent… financial literacy education in schools is very limited and how to grow your money is definitely not part of the educational system.

That is one of the reasons why we started our blog as we see too many people around us with poor financial literacy skills. They have no clue how to grow their money and just continue to put their money on a savings account. Will they teach their kids to do the same and lose money as a result too?

At the end of December we gave our 3rd financial class with the kids. Actually this time the class was repeated twice. One time I gave it to my 13 year old son alone and the second time I gave the financial education class to my wife’s son, her 20+ year old brother and his 20+ year old girlfriend. My wife’s brother and his girlfriend consider financial literacy very important for their future. As this is not part of the financial education system in their country, they wanted absolutely take the opportunity to follow this financial education class.

Similar like previous financial education classes you can download the Powerpoint presentation in the language you prefer at the bottom of this blog post. The objective of financial lesson 3 is to educate the kids the four layers of the financial pyramid and why they are important. Secondly we define a long-term financial objective for the kids. This long-term objective will be the red line for the financial classes during the next five years. Keep on following the blog and you will find out in the future.

Here you find the explanation of each slide and what the key message is while giving this financial education class to your kids. You will also find this in the Notes Section of each slide. Read below the section of what my students think about this class.

Slide 1 : Your Financial Pyramid & Creating a Financial Plan

The goal of today’s financial class is to learn about the financial pyramid. This pyramid is the concept and methodology to manage your money now and in the future. We will also learn how to make a basic financial plan.

Slide 2 : What do you remember from last financial classes ?

First of all let’s see what you still remember from previous financial education classes? Tell me what you learned during Budget Fun and The Compound Interest class. Do you still remember the three key components of the compound interest?

Slide 3 : Exercise 1 : Let’s repeat Compound Interest

Let us repeat an exercise how to calculate the compound interest. You get 10.000$ and you want to grow your money with 7% per year. How much will you have at the end of year 10? Can you calculate me the correct amount?

Did you know that the majority of young people do NOT know the principle of compound interest? It is one of the most important financial concepts to understand!

Slide 4 : Answer to exercise 1

Let’s check your answer and let’s see if you calculated correctly. Give me some conclusions from your calculations.

Be aware that as the amount of years increases, the amount grows exponential and you get a snowball effect where the amount grows exponentially.

Slide 5 : Key Principles of Compound Interest

Let’s repeat the three key principles of compound interest. The first one is the annual rate of return or growth rate of your money. How fast can you grow your money ? The second one is TIME. You need to let time do its work and grow it over time. The third and also important factor is your additions to your total amount per year. You can see the effect on the graph. Over time the amount compounded grows exponentially…do you understand this?

Slide 6 : Why Financial Education is important…

Why is financial literacy important? Too many young people have a lot of debt. Did you know that the student loans in the USA totals up to 1,3 trillion dollars…isn’t that freaking high? After you finish university, you need to work several years to pay off your debt…how painful is that?

Many millennials never got financial education, not did their parents? Did you know that 30% of Americans cannot pay an unexpected bill of 400$ in a month? Don’t become a slave of debt and paying off your debt. Invest in your financial education.

Slide 7 : What you will learn today

Today’s lesson is about the financial pyramid. In your life from young age you need to build out your financial pyramid. You need to execute this step by step. Then we will discuss a basic financial plan. Money is a tool that you can use and need to put at work wisely. Ask questions if you don’t understand something. There are no stupid questions…you only stay stupid if you don’t understand and don’t ask. Learn and have fun!

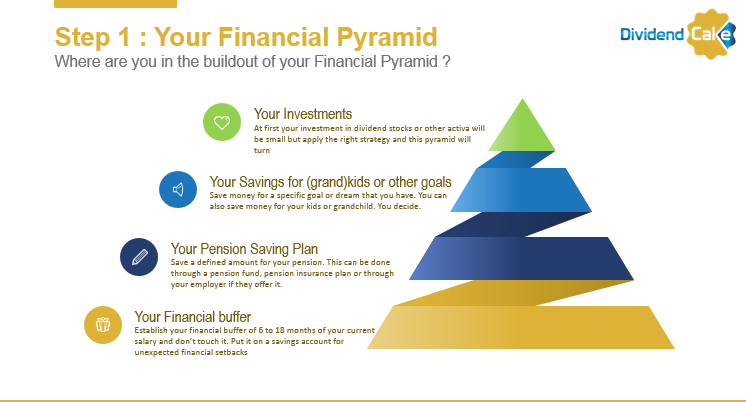

Slide 8 : Your Financial Pyramid

Let’s begin with the first layer of the financial pyramid. This is the foundation of your financial future. This layer is called your financial buffer or emergency fund. You need to build this financial buffer first before anything else. Got it?

Slide 9 : What is Emergency Fund ?

An emergency fund is money easy accessible on a savings account for any emergency that may pop up in your life. You may lose your job, need to fix your car, have to replace a wash machine, pay a high medical cost, whatever in your life that may pop up. You need this financial buffer for emergencies.

So how much money do you need for this emergency fund?

Slide 10 : How much money in your Emergency Fund?

An emergency fund is a multiplier of your monthly current salary. When you are in your 20’s, your emergency fund does not need to be as high as when you are in your 40’s and married with kids. Here’s a basic rule that you can apply. You need between 6 to 14 months of your monthly salary as a financial buffer or emergency fund. Read the example and you know how much you need to save.

You need to complete this financial buffer before moving on to the next layer of your financial pyramid.

Slide 11 : Your Financial Pyramid

Let’s move on to the next layer of your financial pyramid. Your pension saving plan. Governments are paying less for pensions. In some countries parents depend on their kids for their retirement. They receive very little pension or no money from the government. In Belgium the government has failed badly in creating a sustainable pension payment plan for future generations. So you have to take care of it YOURSELF from young age.

Let’s explain in detail why it is important.

Slide 12 : Why do you need a Pension Saving Plan?

Let’s take a look at some numbers. What will your pension be after working 45 years? Take a look at the graph. If you work as an employee, you will receive 1177 euro. And you need to work until the age of 67. But who says that this age will not increase before you become 67. Maybe in the coming 10 or 20 years, the retirement age will become 70 years old.

If you want to travel or need to pay medical care, that pension will soon appear not to be sufficient. Start saving from young age a percentage of your monthly salary.

Slide 13: Why do you need a Pension Saving Plan?

Make sure you don’t have financial problems when you are old. Create a solid financial plan. Did you know that more than 25% of retirees in the US is still working as otherwise they are bankrupt. They still are paying off debt. In Belgium you need to make sure you have extra income from other sources so you don’t become dependent from money from your kids. If you can not pay a pension home, the government will sell your house or ask money from your kids !

The government can ROB all YOUR money !! Be aware !! Make sure you have a plan where you can retire as soon as possible.

Slide 14: Your Savings for (grand)kids or other goals

The next layer in your Financial pyramid is saving for specific goals. Put a % of your salary aside for an objective that you want to save for. Put this money on a separate account that you will NOT touch until you use this money for this objective.

Tell me some objectives in life you have…

Slide 15 : Why do you need to save for Specific Goals ?

Some examples of longterm goals. At the age of 18, you might want to buy a car. At the age of 20 you may want to travel Europe or in the world. You may want to visit the Taj Mahal in India. This is for me the MOST BEAUTIFUL wonder and building in the world. Incredible how they build this ! You need to see it !

Maybe at age of 30 or older you want to buy a house or apartment. Maybe you have another dream…

Slide 16 : Why do you need to save for Specific Goals ?

How can you save for specific goals ? You pay yourself first each month ! You put a % of your salary aside from the monent you receive it. For example. You have a salary of 2000 euro. You put 120 euro on a savings account each month !

Focus also on spending your money on experiences instead of things. It’s better to tell a nice exciting experience than bragging about the purchase of a “material thing”.

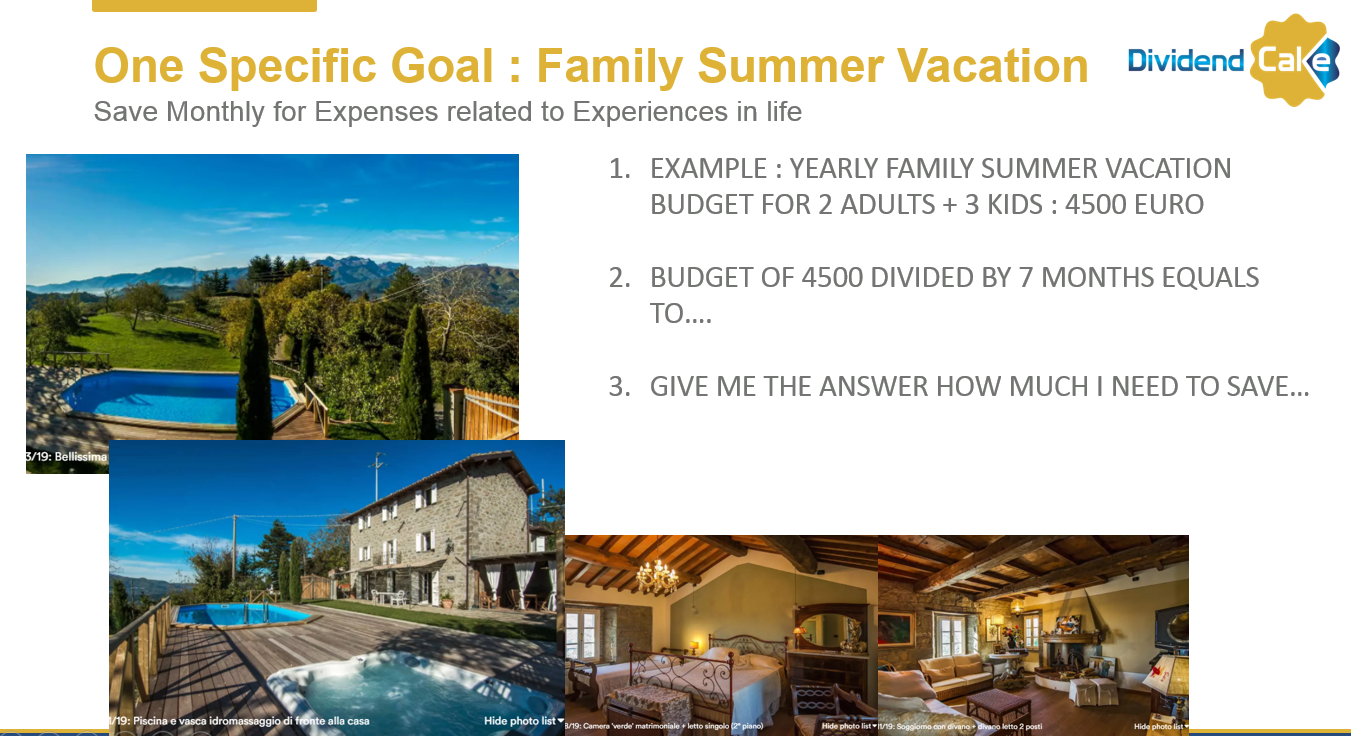

Slide 17 : One Specific Goal : Family Summer Vacation

Let’s use an example. If you want to do a yearly summer vacation, you need to save money, right?

Let’s use an example. If you want to do a yearly summer vacation, you need to save money, right?

A family of 5 (2 adults and 3 teenager kids) can require a vacation budget of 4500 euro. Here you see pictures of the vacation house we will rent in 2018. If you know you need 4500 euro, how much do you need to save each month in order to be able to pay this rental vacation house and expenses locally? Give me the answer…

Slide 18 : Your investments

The last layer in your financial pyramid is your investments. This is the layer where you will grow your money. All money that pay yourself in your investment account goes here.

Please know that the banks, nor schools will teach you how to grow money. Many people know how to put money on a savings account where you lose money. But not many people knowhow to grow money. It will be VERY IMPORTANT TO LEARN HOW TO GROW MONEY !

Slide 19 : Why do you need to Grow YOUR MONEY ?

BANKS do NOT help you to grow your money, they SELL financial products which gives them most profit and the banker a nice financial BONUS…Today on a savings account you get 0,11% interest rate…you get poorer..

Your money NEEDS TO GROW each year !! And you are responsible for this. Otherwise you will work until you die.

LEARN HOW TO INVEST and DO IT YOURSELF ! WE WILL TEACH IN FUTURE CLASSES

Do you know what Warren Buffet says. Never depend on one income. If you lose your job, you are screwed. Make sure you create a second income. How ? We will teach you in future classes.

Slide 20 : Now let’s create a Financial Plan

Now let’s pick a longterm financial objective. You are 13 years old today and enjoying life. In 5 years time you are 18 years old. What could you start saving for?

Let me pick an example. You can start to save for drivers’ classes. 40 hours cost 2500 euro. You can save for a second hand car with a budget of 7500 euro. In total this is 10.000 euro, right ? You need this money within the next 5 years. This is an example of layer 3.

Your current income is money you receive from parents or grand parents today…

Slide 21 : Now let’s create a Financial Plan

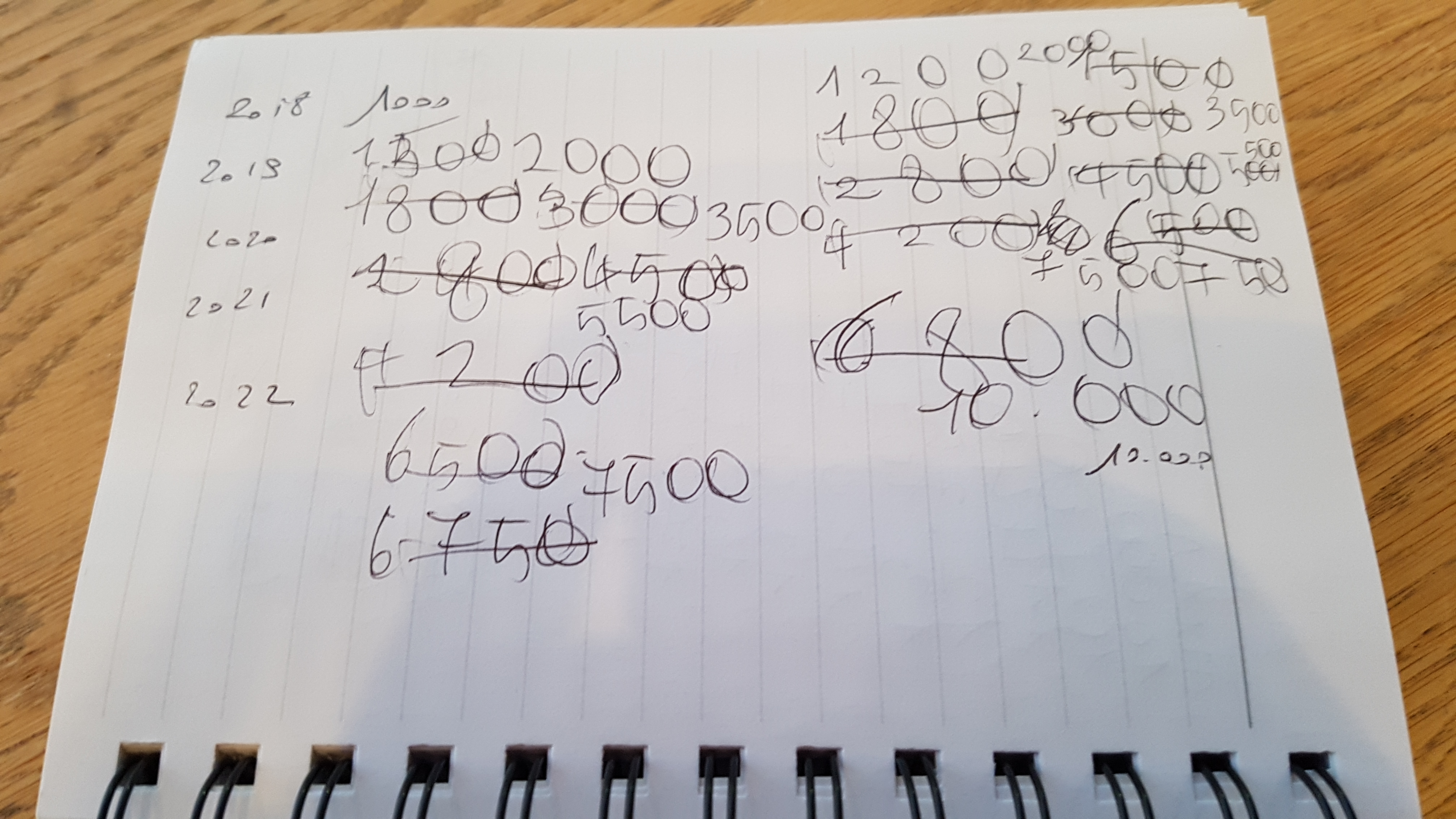

Now what will happen in 2018 ! In 2018 you receive from me a STARTING CAPITAL of 1.000 euro. Your goal in the next 5 years is to grow this 1.000 euro into 10.000 euro within 5 years.

I will NOT BUY a car for you, neither pay your driving classes. It is YOUR objective to grow this money and pay yourself these drivers’ classes and buy your car.

How can we do that ? Let us do some brainstorming…

Slide 22 : Exercise 2 : Let’s fill in YOUR PLAN

Here you see a financial spreadsheet by year. You start with 1000 euro and at the end of year 5 you need 10.000 euro. How do you want to grow this money ? Fill in by year how much hypothetical you want to add each year…

It is not important HOW. Just fill in your assumptions by year and think what you could do to grow this money

when you are older…

Slide 23 : Exercise 2 : A Financial Plan

Here’s an example what I did fill in…At older age you can learn how to invest your money in the stock market. You can also do little jobs on the internet with skills you have, you can do a vacation job at the age of 17…

There are many possibilities…tell me some of your ideas.

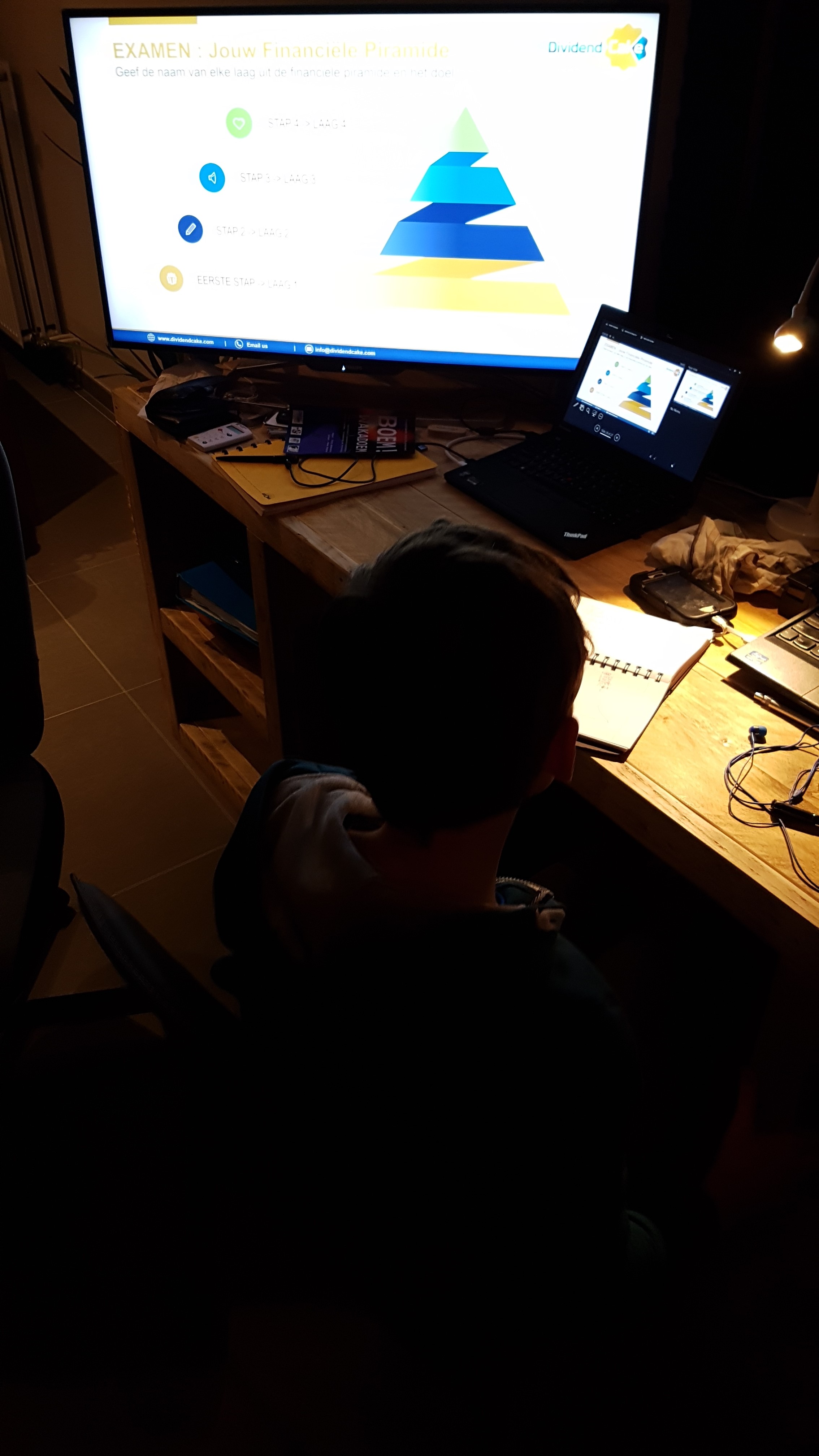

Slide 24 : FINAL TEST : Your Financial Pyramid

Now let’s see if you have learned something today. EXAM TIME !!

Describe each name and purpose of the financial pyramid.

Slide 25 : ANSWER: Your Financial Pyramid

Here’s the answer. Let’s review your answers.

Slide 26 : Final feedback

Let’s talk openly what did you learn today? Give me some feedback. Was this useful for you ?

Slide 27 : Keep on learning EVERY DAY

Never stop learning as this is important in life. Follow your passions and learn, learn, learn…

Feedback and Key Learnings from my students

Getting teenagers engaged for a financial education class may be challenging. When I ask other parents what they do for their kids related to financial education, I get answers like “why (should I)?” or “how” or “my kid is not interested”. Before Christmas I reviewed what learning content my 13 y old son will get at school…

He will get the basics of economics and money. In addition he will learn how the government receives money…and if the government will be able to pay everything? Later in the year I am curious to see that chapter…lol !

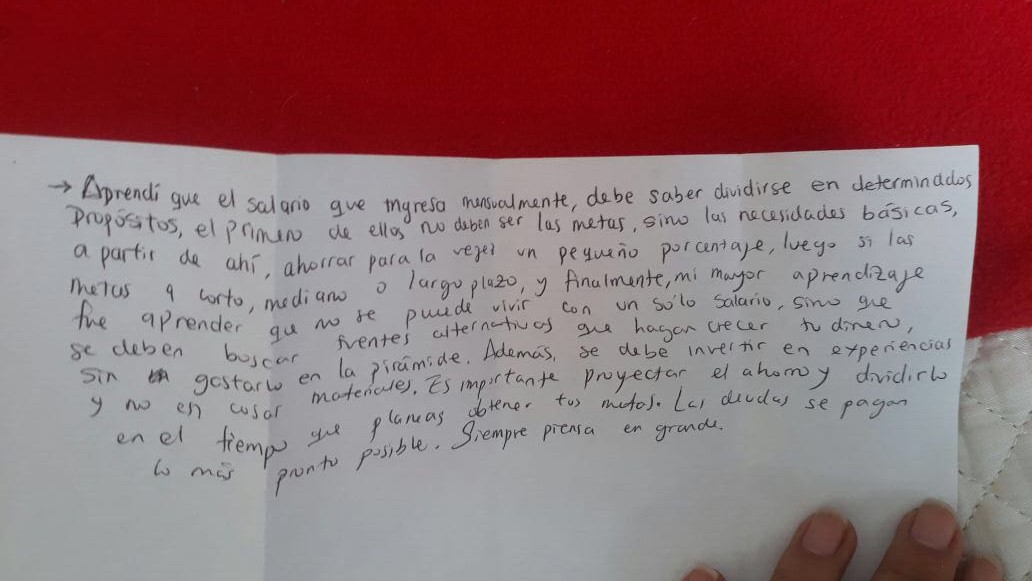

My wife’s son, brother and his girlfriend were very motivated in class. They realize the importance of financial literacy. Below you can read the key learnings from one of my students (in Spanish)

The message basically summarizes the key insights of the class and the importance of creating a second income after paying yourself first and spend money on experiences instead of things.

My son understand the importance of the class. He said…so I have to climb a pyramid. I said..yes. you are correct. When you use your money, you climb a pyramid. How can I grow my money ? I said…we will learn in future classes. Other smart questions I received from all my students :

- Why do women get so much less pension?

- How can I pay myself first ?

- What do I do when I stil have to pay a student loan?

- What percentage do I put aside from my salary?

- ..

Our presentations

Download here our material

DividendCake_Kids Financial education Class 3

DividendCake_Kids Financial education Class 3 – Dutch

Final Words

So here’s the deal we made with our two sons of 13 year old. In 2018 they will receive 1000 euro on an investment account and the goal is to learn how to grow this money to 10.000 euro. The deal is clear…I will NOT pay for a car, not drivers’ classes…

In the next 5 years I will use this objective as an anchorpoint to teach entrepreneurship, investing in the stock market and many other topics.

The challenge you will face as parent is that the world a 13 year old lives in, is all about hobbies, social media, gaming, friends and TV,.. It is very distant from money and financial responsibilities. You need to engage them in the conversation and the learning path. It is not easy to do this..I realize !

But hey…do you want your kids to learn financial literacy from school ? They will get the basics, sure. But that does not mean they are prepared for life. I believe there is a BIG disconnect between the school system and what is needed for teenagers and adults from a Financial literacy perspective.

With our blog, we can do our impact in helping to change that ! Thanks for reading and following us on Facebook and Twitter.

As usual we end with a final quote.

5 Response Comments

Nice presentation. All the best with your kids education.

Thank YOU ! A lot of work to prepare but all worth it !

my child is almost 10 and we are still at the level to practice the weekly “budget” , monthly budget. But I keep your financial lessons for teenagers because is exactly what we will need in 5 years!

Don’t wait 5 years…our sons are 13 and we started at age of 12. More classes are coming this year. Keep on following us ! Thanks

I’ve been absent for a while, but now I remember why I used to love this website. Thank you, I’ll try and check back more often.