Recently I got the question from a student: “I’m in my early 20s and want to get a head start on financial success, but I don’t want to make mistakes that could prevent me from achieving my goal. What do you suggest?”

Below are five financial mistakes with the capacity to seriously undermine your economic prospects. Avoid these major missteps, and you’ll dramatically increase your chances of achieving financial success and growing your net worth. Your goal should be to become financially independent as soon as possible.

Mistake #1: Getting A Late Start On Saving.

More than any other single error, I’d say this is the one that prevents people from attaining at least a measure of financial security. For example, in a recent survey of Febelfin 19,7% of those polled said they have not started saving. A 25-year-old earning $30,000 who saves 10% of salary a year would have a nest egg of just over $620,000 at 65, assuming 2% annual raises and a 6% annual return on investments. If that person holds off just five years, the size of the nest egg falls by almost $140,000. Waiting 10 years shrinks it by more than $250,000. Whether this calculation is in Euro, Dollar or any other currency doesn’t matter.

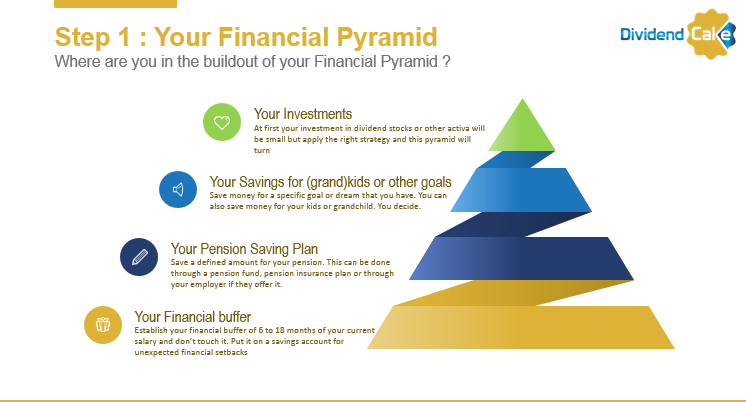

Your first goal should be to build and accumulate an emergency fund of at least three months’ worth of living expenses in a savings account so you’ll have a cushion to fall back on in the event of a job layoff or unexpected expenses. This is the first layer in our Financial Strategy, your Financial Buffer.

The main point, though, is to get into the habit of saving regularly and maintain that regimen throughout your working life.

Mistake #2: Taking on unnecessary debt.

Sometimes it makes sense to borrow — say, to buy a house, purchase a car or finance an education that can increase your earning power. But it’s the debt we take on to maintain a lifestyle that exceeds our earning power that gets us in trouble.

And make no mistake, paying down debt can strain your budget. According to the European Committee for Systemrisks (ESRB) debts of Belgian families are increasing rapidly as families think that they can take 30 year long mortgages to pay off their house. You don’t want to pay off mortgages all your life, don’t you?

Before you borrow, ask yourself: Is this something you truly must have? And if the answer is yes, then ask: Could you get by with a less expensive version of it? And finally, consider whether the monthly principal and interest payments you’ll make for years might be put to better use going into savings and investment accounts that can grow in value and provide a cushion against economic setbacks.

Mistake #3: Buying into Wall Street’s ‘investing is complicated’ mantra.

The message investors get from many bank advisors and media in Europe boils down to this: You need to watch the financial markets constantly, spread your money among all sorts of bank owned and managed mutual funds and be ready at a moment’s notice to dump what you own for new investments. And, of course, to pull off all this successfully, you need their help, for which you must pay a handsome price.

Nonsense. No one, not even market pros, can consistently outguess the financial markets. And research by University of California at Berkeley finance professor Terrance Odean shows that trying to do so by frequent trading is more likely to hurt than enhance your returns.

You’re much better off with a less-is-more approach: build a basic portfolio of broadly diversified stock and ETF’s that matches the level of risk you’re willing to take — and then, aside from occasional rebalancing, stick with that portfolio regardless of what the market is doing.

Mistake #4: Overpaying for financial help.

Whether it’s the annual expenses you pay to a mutual fund manager or the fees you shell out to an adviser to help you choose the right funds and provide other financial advice, the fact is that paying more than you have to drags down the returns you earn and makes it harder for your savings to grow. Which is why it makes sense to hold the line on such costs as much as possible.

When it comes to investments, the easiest way to rein in expenses is to stick as much as possible to low-cost index funds and ETFs. Doing so can easily save you upwards of 1% a year compared with the typical stock mutual fund.

If you feel you need to work with a financial adviser, make sure you know in advance exactly what you’ll pay, what specific services you’ll get for your dough — and comparison shop to make sure the fees the adviser you’re considering are competitive.

You may be better off signing up with a “robo-adviser,” an online service that uses algorithms to provide inexpensive investing advice. Examples are ETFmatic, Trigger, and others…

Mistake #5: Failing to monitor your progress.

You don’t have to (and shouldn’t) constantly obsess about money matters. But neither can you just set a course and then assume all will be fine going forward. You need to periodically review your finances — say, once a year or so — to ensure you’re making headway.

The most comprehensive gauge of whether you’re making progress is to track your net worth — that is, the difference between the value of your assets and liabilities, or what you own vs. what you owe. You can use our Financial pyramid to track your money assets.

If you’re saving regularly and investing sensibly, over time your net worth should grow. If it’s stagnating, it may be a sign that you’re not saving enough, not investing your savings sensibly or taking on too much debt.

You can estimate your net worth using this simple net worth calculator. By doing this calculation every year and comparing the results to those of previous years, you can easily see whether your net worth is growing.

Clearly, there are also many positive steps you can take to enhance your prospects, one of the biggest being to nurture your career so that you can earn (and save) more during your working years. But good defense still counts for a lot. And if you avoid making the five mistakes above, you will dramatically improve your odds of achieving the financial success you seek.

Final comments

Read our Financial strategy and build your investments in the four layers of the pyramid.

Don’t put yourself in debt for a house from young age. But build first that cushion and financial buffer. Then start planting those fruit trees (stocks or ETFs) that will give you fruit (dividends) every year. Pay yourself first and don’t make any of the five above mistakes. Create that second source of income !!

If you follow this advice, I am sure you will be able to retire earlier than the retirement age. Wish you good luck with the execution of your personal finance strategy.

European edited version of article on CNN Money

No Comment

You can post first response comment.