Life is more than earning cash flow. My mother has finally left the hospital and recovery home. Now she is back home. It’s those moments in life you realize there are sometimes other priorities than earning cash flow and writing a blog post. I hope you understand why my blog post writing past weeks has been limited.

In a column on Marketwatch.com, Paul Brandus discusses the fact that we are in the biggest bull market ever but still a disaster looms for millions of retirees.

First the good news: As you know, the stock market has surged for more than a decade. Since the recession low of March 9, 2009, the S&P 500 SPX, +0.26% has rocketed from a devilish 666 to over 3,000 today. That’s a gain of 350% in 10 years. Talk about building wealth.

Now the bad news: This incredible period of wealth creation has bypassed tens of millions of older Americans — perhaps including you. That’s because — get this — the wealthiest 10% of households own 84% of all stocks—and that includes pension plans, 401(k) accounts and individual retirement accounts (IRAs) as well as trust funds, mutual funds and college savings programs like 529 plans. That means 90% of American households own the remaining 16% of all stock.

These sobering stats come courtesy of Edward N. Wolff, an economist at New York University, who tells the New York Times “For the vast majority of Americans, fluctuations in the stock market have relatively little effect on their wealth, or well-being, for that matter.”

And it’s not like older Americans had a little bit saved a decade ago and made some gains — maybe a few hundred or a few thousand dollars — over the past 10 years, but not enough to make much of a difference in their lives. Many have — literally — nothing. According to the U.S. Government Accountability Office (GAO), nearly half of Americans aged 55 or older have nothing set aside in a 401(k) or other individual account. Nothing. The adage that the rich get richer and the poor — well, you know the rest — certainly seems true.

Of course individual savings are, or should be, only one source of income for retirees. Pensions and Social Security are the others. But three-fifths of such households — again headed by someone 55 or older — do not have a traditional pension. This leaves Social Security, which, as we’ve explained many times before, has troubles of its own.

And remember: Social Security is only supposed to be a supplement for pensions and personal savings — yet more than half of senior households rely on it for at least half their income. Up to a quarter of them rely in it for 90% of their income — a near total dependency.

Adding to senior woes is growing debt. In 2010, says the National Council on Aging, 51.9% of households headed by an adult aged 65 or older had some debt. Just six years later that percentage had jumped to 60%. The median level of that debt in 2016 was $31,300 (median means half have more debt than that half have less).

All of this helps explain how utterly unprepared tens of millions of Americans are for retirement, and why many in fact, will never retire at all — at least not in the way they probably envisioned when they were younger. I call this, perhaps with a bit of hyperbole, a “tsunami of poverty and deprivation” that is fast approaching and seems unstoppable. A 350% stock market gain offered the opportunity to flee to higher ground, but most missed out.

“The problem now is that many years have passed, and that means less time to make up for lost ground,” says Reginald Nosegbe, chief executive officer of Valspresso, a fintech and investment strategy firm based in Reston, Va. He warns that older people trying to make up for retirement shortfalls may move into riskier assets — at a time in their lives when they’re supposed to be dialing back risk. That’s if they even have assets to invest in the first place, of course.

“It’s always a good time to save and to invest,” Nosegbe says.

So let’s see what our September & October 2019 cash flow was for my mom’s portfolio.

Passive Income in September & October 2019

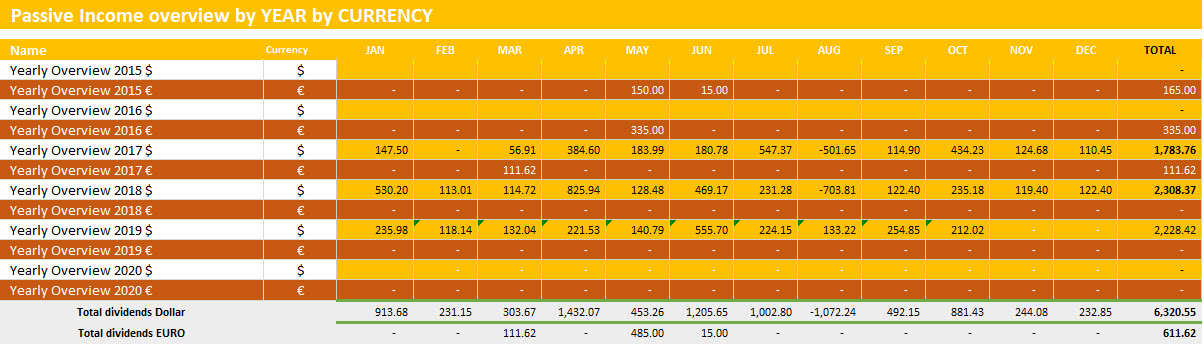

During the month of September & October 2019, we received in total 466,87$ passive income. We received 120$ for 1 options trade. In total we received 2228,42$ for the year 2019.

Here you find the overview of all passive income payouts during the year 2016, 2017,2018 and 2019.

We have now 63% of our yearly objective.

The Options Trade Review

We sold covered calls on our AGQ position and received 120$.

Going forward

Achieving an average options premium income of 300$ per month in times with other priorities was past months quite difficult. Let’s achieve the maximum we can achieve the next 2 months…

In 2019 we will send out ONE newsletter per month to our blog followers. Life can be busy sometimes and people lose track of following a personal finance and travel blog. Subscribe and you will get one email per month highlighting what you missed…

Thanks for following us on Twitter and Facebook and reading this blog post. We end with a quote as always.

Source :

No Comment

You can post first response comment.