A few times a year I try to slot in an investors or trading event where I can learn the latest economic insights and/or new investor strategies. VFB Trefpunt Leuven organized an interesting agenda “Fundamental Analysis” day full of different investing topics. More than 200 interested investors sacrificed their Saturday to attend this event. Below you can find our summary.

Fundamental analysis is looking how a company operates within an (global) environment and how it’s business model evolves over time and how this company is earning money. Whether it’s real estate, energy companies or small caps, you need to understand many key factors that influence the balance sheet of a company. It all starts with the economy !

Economic Outlook 2020 by Koen De Leus (BNP Paribas Fortis)

Koen opens with the statement that it’s pleasant to present for investors who don’t need to be convinced to invest in the stock market.

The macro environment outlook starts with the US elections of President Trump in 2020. The US economy still performs good. The unemployment rate is decreasing. This always indicates that the current president can be re-elected. The chances that Mr Trump will be elected again, is very high.

The tax cut has lifted GDP by 0,7&% on average in 2019 and 2020. Positive effects of corporate tax cut are unfortunately offset by negative effects of the trade war. The uncertainty that this has caused in the global economy, is the highest since 1970. This uncertainty has a price of 1% downwards on the economic growth. The big question is “Where are the next Tariffs?”. The global trade war can go on for another 10 years. The car industry is in total decline with the transformation towards electric cars. The vehicle demand is in decline.

How about Europe? Not so good. An economic growth of 1%.. The trade balance of Germany has been growing. The other countries are mostly flat. This makes the European economy vulnerable. The past years the consumption and the company investments has been positive. In Q2 2019, you notice a lot of company investments but the net export has declined significantly. The ECB keeps the interest rates low and people are saving more money as a result, most likely for their pension.

How about Brexit? When the conservatives win the elections and have a majority, there can be an end to Brexit at the end of January and the start of a new trade agreement. A transition period will be required in this scenario. When the Labour party wins, there will be a softer Brexit or remain. The stock markets will react negative on this outcome. A second referendum will lead to the possible independence of Scotland and the break up of Great Britain. (We know now that Boris Johnson won the elections and the markets responded positive)

What about China? China accepts slower growth. Shadow banking contraction is about to reverse for sectors where the banks want to give credit. The Chinese president Xi wants a stable economic growth and lifts the world GDP growth. China has been investing heavily and their debt has been growing. Japan and Australia have also been investing the past years. It is the ideal time to invest in other countries.

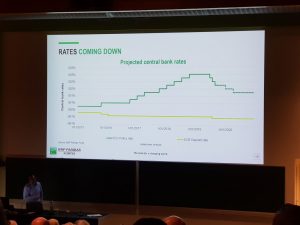

What’s the outlook? We will see slower economic growth. Oil will be dropping in price due to shale production. We are still in low interest rates climate. Next year we can expect two more Fed interest rate decreases. The economy will slow down more so more interest rate decreases will be needed.

Shadow rates in Europe are minus 7%. Before an interest rate increase, we will need to absorp all the negative rate. So interest rates can remain a LONG TIME negative in Europe. The dollar will remain strong. Cash is not the answer and inflation is eating away your purchasing power… So savings accounts are not the answer. We can have another stock rally if there’s a China trade deal. We keep on printing more money… equal as the height of the statue of Liberty…

What to invest in those days? Well, prices for FINE ART are booming due to liquidity in the money market. How about gold? We see that gold will increase to 1600 in 2020. 2.000 is the midterm target. There’s plenty of upward potential.

How about interest rates? The ECB wants to increase the credit going forward with low interest rates. A lower interest rate doesn’t help the confidence. The real interest rates globally has evolved from positive 6% to negative. Japan, VS and Euro zone has a falling equilibrium interest rate environment. It is more and more difficult to stimulate the economic growth. So, there’s more inequality!

How can we change this? The last 10 years the governments have invested too less enough. If we loan 1% more, what would this mean? The impact is 4 times on the economy. We are entering a new world with low inflation, global trade wars and countries adding new walls.

Outlook in the energy sector by Eric Bosman (VFB)

After World war II the energy sector knew three periods: a regulated controlled environment mostly owned by the government, privatizing of the market players and regulated net operators, and the prosumer (contamination of producer – consumer) era where production is more decentralized with new products and services of the commercial energy players and net distributors.

Today we are in the third phase and period called “Energy as a Service”. When you review a regulated energy company, you need to analyze and review the ROA (return on assets). This period has led to a mature energy trading market. The global energy markets are fully connected. For example : If coal can not be exported from Australia, coal prices will increase and electricity prices will increase as a result. Germany is still dependent for the next 20 years on coal power energy electricity stations.

Today we are in the third phase and period called “Energy as a Service”. When you review a regulated energy company, you need to analyze and review the ROA (return on assets). This period has led to a mature energy trading market. The global energy markets are fully connected. For example : If coal can not be exported from Australia, coal prices will increase and electricity prices will increase as a result. Germany is still dependent for the next 20 years on coal power energy electricity stations.

Eric explains the Asset and Liability Management model (ALM) of a bank for proper risk management on assets. Also utilities use a profit and risk management model. Today you can become a energy consumer and producer. Battery storage becomes much cheaper and as a producer you can decide when to sell your energy to the market. Prosumers model has completed changed this market place.

What business models of new producers and consumers are emerging? Blockchain technology, decentralized production and micro distribution are in constant change.

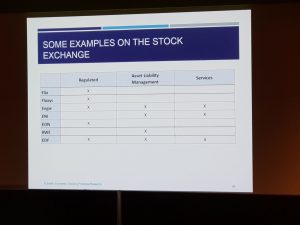

We can summarize that distribution nets are regulated for off the shelf STEG and photovoltaics, wind and battery nets. Energy production and sales have central risk management model. To illustrate these business models with companies on the stock exchange, take a look at below overview of stock listed companies.

So how do you analyze an energy company? You need to review the relative weight of the company’s business model and its profits evolution. Secondly you need to know the hedging policy if you need to pay a tax. (Nuclear tax based on 1-3 year spot). Eric ends his presentation with a comparison charts between Fluxys and Elia, RWE and Eon, Electricite de France and Engie and commodities prices.

He highlights a small cap example, that is named 7C Solarparks SEO. Eric ends with the statement that the S&P index only contains 5% energy stocks and that you always review the business model of a company to evaluate an investment.

Real Estate Investment Trusts (REIT) by Gert De Mesure (VFB Analyst)

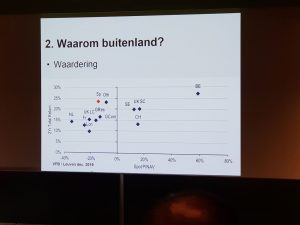

REIT (GVV) investments exist in 40 countries worldwide. Why invest in foreign REITs? The main reason is spreading and diversifying your risk. There’s a bigger chance on an acquisition of a REIT. Last year there were 4 out 10 acquisitions. If you look at below chart, you immediately notice that Belgium REITs are really high priced due to great performance. All REIT returns are between 8 and 20%. Other countries have still upward potential.

What you need to evaluate is the dividend performance. In Belgium the average dividend return is 4,5% and 20,5% price value increase. What are we looking for? We avoid a REIT that simply purchases for the sake of buying. What you need to look for, are developers that innovate and develop their know-how in certain markets.

There are two risks : the interest rate long term and inverse return OLO on 10 years. Another risk is the correlation with the stock indices. Don’t buy the big REIT, but search for the smaller caps who have less risk. Take a look at our current selection. Two are already acquired by other companies.

Let’s review those REITs.

Coima Res is an Italian REIT with a focus on Milan. It’s a young company with money from Qatar and they have developed in a very dynamic market of Milan. You can purchase this REIT at a high discount.

Deutsche Wohnen is one of the biggest German REITs with 168K houses, 2,8K shops and 89 pension homes. Stable growth, frequent renovations and real estate services are their strengths. 70% is based in Berlin. The debt ratio is 38% and the stock price currently rates at a discount of 15%. Dividend ratio is 2,7%.

Grit is a small cap in Mauritius with South African pension funds money. There’s little risk on the current assets as it is geographically diversified. The stock is listed at the Johannesburg stock exchange. Tenants of their real estate are mainly international groups in the pipeline industry with a sale and lease back model. The dividend return is 10,2%.

Olaf Thon Eiendomsselskap is a Norwegian portfolio with 78% shopping malls. The stock price has significantly grown. The dividend return is poor with 2,8%. Patrimoine & Commerce is a French group in low cost retail parks. It currently lists at a 31% discount and has a dividend return of 7,1%. The company is growing but the stock price is not following yet..

Regional REIT is an UK REIT active in business real estate, industrial real estate and shops, mainly in big cities (not London). In 2018 the performance was strong due to great sales. The dividend return is around 7% and has been stable the past 5 years.

Conclusion : Belgian REITs are not cheap…this doesn’t mean you need to sell those REITs. Search abroad cheaper alternatives with more stock capitalization potential. Focus on value creation companies. Follow the research on Gert’s website. Always diversify your REIT investments is Gert’s KEY MESSAGE.

Find the presentation under vastgoedbeleggingen on the URL: www.gertdemesure.be

Higher Return with Small Caps? – A Benelux selection by Hans Heytens (Merit Capital)

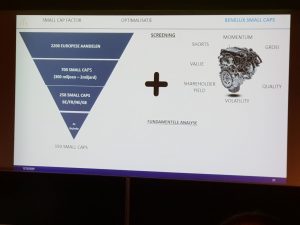

The goal of the presentation is to review the small cap sector and how we can optimize our strategy. The small cap factor are stocks with ONE COMMON characteristic. It’s a unique source of return and risk that differ in return. Can we earn a return if we invest in a portfolio of small caps? Are investments in small caps long term sustainable and robust enough? Small caps are companies below 300 million.

A study paper of Rolf Banz says you can earn 5% yearly if you invest in the 50 smallest companies. Another paper study says it earns only 3,1% yearly. Another study concludes a return of only 1,8%. If we review the long-term performance of small caps, there’s no consistent return or no return at all…

- Conclusion 1 : If you invest in small cap ETF, there’s little proof you can earn a return

- Conclusion 2 : A tactical allocation can be interesting. It depends on the momentum of the small cap. Execute a technical analysis with a trend identification. Also look at the macro environment.

The current momentum for small caps is negative. The dividend return is improving. The current discount is 12%. In the future small caps can become interesting for an investment.

How can you optimize a diversified small cap portfolio? “Size matters, if you control your Junk”. You need to focus on Quality with profit ratios (ROE & ROA) and cash flow. Is there growth with increasing cash flows? What is the risk (debt, leverage) and payout ratio?

Conclusion 3 : Structural investments in quality ETFs can be interesting. You can screen your quality in the following stock screeners :

After screening 2200 European small caps on different parameters, we can review 5 potential investment ideas. There are 2 small caps with momentum and better performance (>70%) than others. Hans reviews the 6 different momentum parameters. The two investment momentum ideas are Lotus and Orange.

If we perform a Quality Value Screening, we search for TOP quality investments at fair value. Combined with fundamental analysis parameters, we find the company Gerard Perrier Industries.

We conclude with a shareholder yield screening, dividend yield + buyback yield. We search for high shareholder yield, low volatility and strong quality. This results in two companies. The first one is CFE with a dividend of 2,8%. The second one is a French IT consulting company Assystem, who is active in different sectors. The dividend is 3,7%. Both companies have growth potential. In the presentation you can find more small cap listings to review potential other investments.

Dividend Stocks – Opportunities and Traps by Geert Campaert (Dierickx Leys Private Bank)

Bonds market has completely collapsed. So investors are searching for alternatives. One alternative is dividend stocks. The first key question is the dividend sustainable going forward.

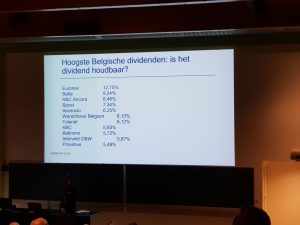

Look at below Belgian dividend stocks.

Geert doesn’t consider the EURONAV dividend trustworthy. Same story for Balta which stock price collapsed from 12 to 2 euro after the IPO. BPOST has also a declining dividend as a result of declining revenues and profits. Telenet doesn’t have a trustworthy dividend policy either. Proximus has the same challenges as Telenet and the dividend has only been kept thanks to the Belgian government shareholder who needs the money.

The second question is the NAV – Net asset value of a company compared to the stock price. So would you invest in a company where you pay a premium versus the NAV ?

The third question is: how does a company score on ESG (Environment, Social and Governance)?. If a company scored bad on these parameters, fund managers will sell those companies. An example are big banks with a high dividend but poor ESG score. Examples are ABN AMRO, Danske Bank Nordea and SEB, all banks named in money laundry cases. Another example are oil producers with high dividend and poor ESG scores. Shell, BP and Total stock prices have been under pressure.

Here’s the selection for dividend stocks

- AGEAS : insurance companies with a growing dividend and strong market position

- GIMV : investment company with a big cash position

- TINC : portfolio of infrastructure projects with long-term contracts and predictable cashflows.

- Confinimmo : REIT with gross dividend return of 4,23%. Current premium is 31% on NAV.

Debt – a blessing or a curse by Pascal Paepen

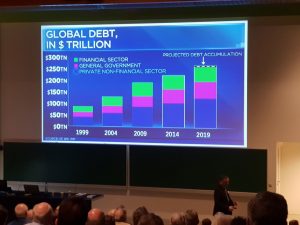

255.000 Trillion debt is growing every day. We are addicted to credit! Do we have to be fearful or can we have a party?

Government debt is perpetual and current interest rates are extreme low. Government are being paid to behave badly. Central banks want to create an inflation of 2%. Now it is a goal. Transfers are also occurring between countries to avoid bankruptcy in one country. Savers will be victim for all this government debt.

Companies are owned and supported by bond investors and shareholders. Those two parties have conflicting interests. If things go wrong, there follows a financial restructuring with (partial) debt liquidation. We have seen this in Greece and also for the company Exmar.

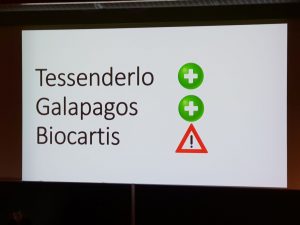

How can you protect yourself as an investor when you invest in a company? A few examples ..

Tessenderlo : 600 million bonds and other credits that expire within 18 months.

Galapagos : IPO for 22,4 million

Biocartis : may 2019 Biocartis released a convertible bond and stock price dropped with 13,5%.

A few examples where the financial situation went wrong…

- Nyrstar : Buying mines to become independent of suppliers… There was a huge conflict of interest

- Fortis in 2007… a known story. Acquisition of 72 Billion for ABN AMRO with 24 Billion debt for Fortis. This was an acquisition where the money was going to come from…

- Parmalat : Beppe Grillo shouted it out on a stage that Parmalat was one big fraud after numerous acquisitions.

- Greenyard Foods

- Heinz Kraft

Telenet is junk, non-investment rate. Telenet has big debt. 7 shareholders positions are from Liberty Global and 3 shareholders are independent. Where’s the money going you think…

Another example is Recticel. In 2007 Recticel released a company bond and one year later they purchased 50% back at half the price. The same happened with Real Dolmen. Sometimes you can find opportunities. An example is Arcelor Mittal. Another one is AB Inbev.

Where do you need to pay attention? Here are the four questions within your credit analysis.

- Who gives the credit and what is the hierarchy? A bank, a bond investor or a company shares investor. A bond investor can sometimes be inflexible and request to be repaid 100%.

- How big is the debt? All debt including leasing debt (AirBerlin). In what currency?

- Cashflow Position to pay debt?

- Spread of the debt in the coming years

Can debt be a curse? Sure. One great example is the house investment of Warren Buffett. He invested 150.000$ with a loan of 120.000 for 30 years. He sold it for 7,5 million last year. The investment of his 120K within stocks of Berkshire Hathaway resulted in a return of 5.000%.

Can debt be a curse? Sure. One great example is the house investment of Warren Buffett. He invested 150.000$ with a loan of 120.000 for 30 years. He sold it for 7,5 million last year. The investment of his 120K within stocks of Berkshire Hathaway resulted in a return of 5.000%.

Pascal ends with the story of AB InBev that grows with debt. The company wants to decrease now the debt position.

Final Note

What did we learn ? The most important part for myself was the economic outlook 2020 by Koen De Leus followed by the REITs presentation of Gert De Mesure. The other presentations learned investors how to evaluate debt, energy companies, dividend stocks and small caps. All those presentations are key knowledge for a (starting) stock market investor. I did talk to some investors and some investors had no stock market knowledge at all. One investor was a bond investor in the past but he realized this strategy didn’t work anymore. One young investor realized his saving account wasn’t giving him any return either… unfortunately still the majority of people save money on their savings accounts as they don’t possess the knowledge to invest wisely in the stock market. Instead of 200 people, the room should have been filled with thousands of people who need this knowledge. Financial literacy is the important skill but schools fail and so do the majority of parents. Banks won’t teach you either. I can only applaud the organization VFB for doing this (ww.vfb.be)

We hope you learned something from this blog post and you appreciate our effort to write up the summary.

Don’t hesitate to leave your comments and feedback. Let us know what you think.

Good luck with your personal finance strategy! Thanks for following us on Twitter and Facebook and reading this blog post. As always we end with a quote.

No Comment

You can post first response comment.