The past months October 2016 to January 2017 have been quite interesting related to the press about Savings accounts in Belgium. I know interest rates in the USA and other countries are also low.

End of October 2016![]()

Suddenly the press communicates that one Belgian bank KBC, changed the conditions of the savings account for all their savings accounts of companies. This allowed them to bring this interest rate to ZERO %. Wow !

The bank communicated later on that in total it related to 6, 22 billion euro. The bank saved itself a lot of money for paying interest of 0,11 on this amount. In addition the same bank KBC communicated that they stop with Start2Save savings account where customers could save up to 500 euro a month for a higher interest rate. The interest rate on this successful product was 0,71% compared to a regular interest rate of 0,11.

December 2016

December 2016

Many banks such as BNP Paribas Fortis lower their savings accounts interest rates to the bare minimum. Also other banks such as Fintro and Rabobank do the same to a low of 0,15%. The difference between the highest and lowest paying interest rate is a ratio of 16, where the highest interest rate you will be able to find on a comparison site such as www.bankshopper.be is 1,5%. The lowest on which the majority of the people’s money is parked at the BIG commercial banks give an interest rate of 0,11%.

According to the most recent data the inflation in December was 2,03% for the year. In 2015, the inflation for the year was at 0,56%. This means that consumption prices for food and other goods are increasing and you can buy less for the same money.

In December 2015 for every 10.000 Euro that was put on a savings account, you lost 135 Euro. See a newspaper screenshot of December 2015 to prove that we are correct.

If you use the yearly inflation rate 2,03% in 2016 and the interest rate of 0,11%, you lost in 2016 192 Euro. That is an increase in losing buying power and losing money without realizing it. You have to make sure that your investments generate money.

So honestly when we hear in the press that the amounts on savings accounts keep on increasing, we really can’t understand why people chose for the solution where they lose money. Is it financial knowledge, advice from the banks, what could be the reason? Possibly people think there is no alternative (TINA).

Dividend Stocks

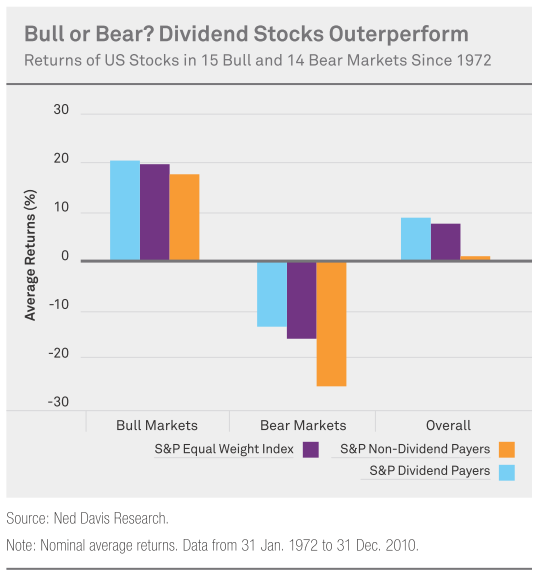

In January we read an interesting article of Ned Davis Research that compared dividend stocks against bonds and savings accounts. The conclusion was simple : Dividend paying shares outperform in the markets. Those dividend stocks can be boring but you still can achieve double digit income growth. A Dividend growth strategy is a perfect way to build a “dividend cash factory”, as we love to articulate it. Here’s a graph of this research

In our Portfolio strategy we focus on three different types of dividend paying stocks or ETFs :

- High Dividend Stocks between 4 – 20% dependent on the strategy (Read here our Strategy)

- Monthly Dividend paying stocks (with a dividend yield higher than 8%)

- Dividend Paying ETF’s with a dividend yield higher than 6%

You don’t have to pick stocks or ETF’s with higher yield than 6%. Some bloggers prefer stocks or ETF’s between 2 and 7%. If you are happy with that kind of return, fine. We don’t make a judgment about it.

Our strategy is all about cash flow! In simple terms money appearing on our bank account… If you want to read how our progress is, read our Yearly Dividend Income page.

We hope you also make your money work for you. Good luck with your financial strategy and education! Educate yourself first!

Keep following our progress. THANKS FOR READING AND FOLLOWING US!

One Response Comment

Dividend stocks are my favorite type of stocks. That chart really shows the Beni fits of dividends. Thank you.