Saturday 13th of May, we headed to Thomas More Hogeschool in Mechelen where the investors organization VFB organized a congress about Financial Planning. This congress caught my interest as it consisted of 4 presentations about 4 different financial planning topics.

Saturday 13th of May, we headed to Thomas More Hogeschool in Mechelen where the investors organization VFB organized a congress about Financial Planning. This congress caught my interest as it consisted of 4 presentations about 4 different financial planning topics.

In an aula filled with around 100 people, Sven Sterckx, chairman of VFB opened the day with saying that financial planning is important for everyone. “Today is all about your net worth and wealth planning”.

The day starts with a presentation of Prof. Emiel Van Broekhoven who will explain Financial planning and why this is needed. He is since 1983 known as the expert in Belgium that placed Personal Financial Planning on the map in Belgium.

Intro to Financial Planning (Prof. Emiel Van Broekhoven)

Financial planning…. The professor starts talking about financial advice and independent financial planners. Today there’s a law to regulate financial planners. This law does not exist in US and other big countries.

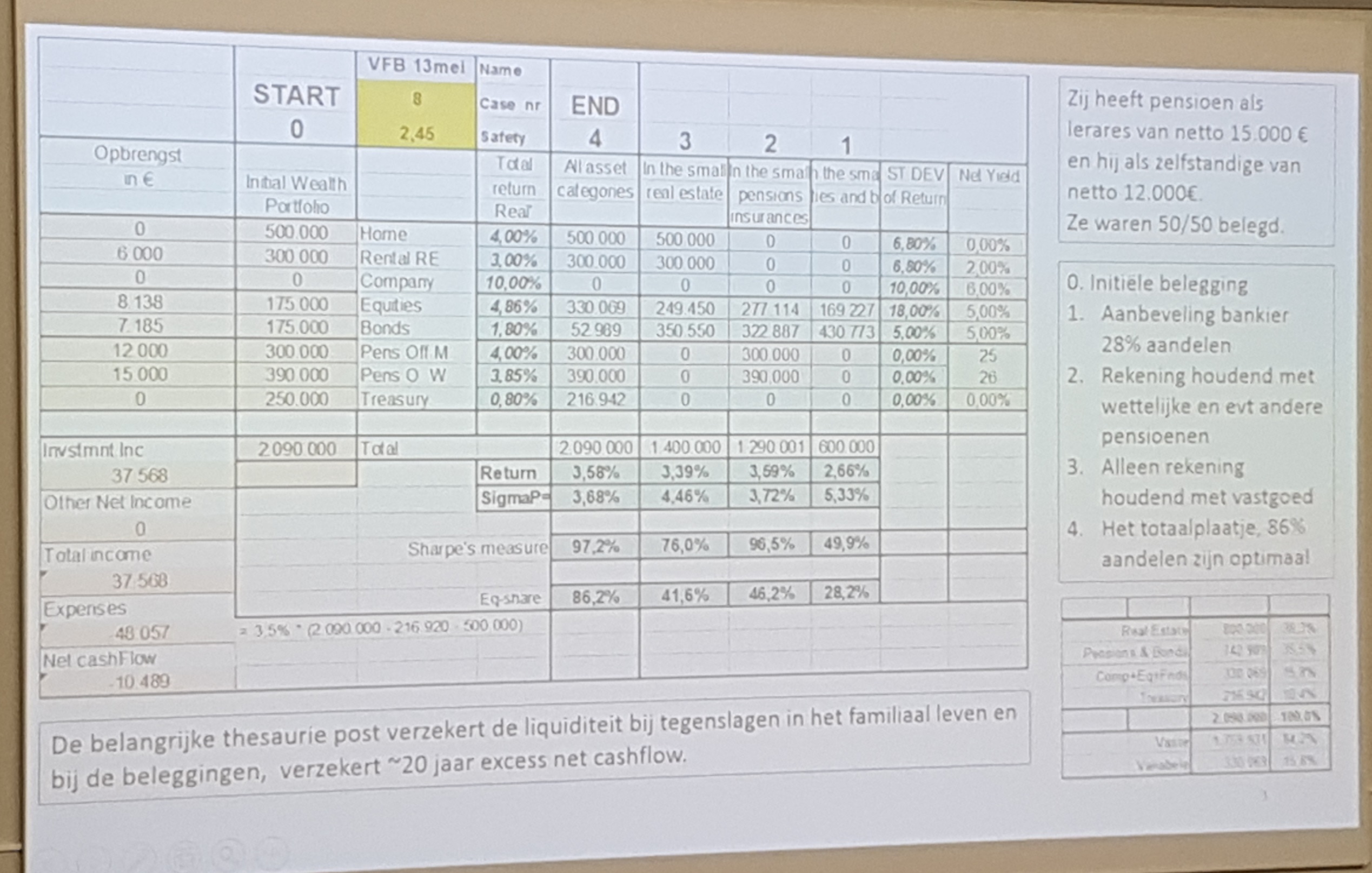

An independent advisor cannot give advice about specific shares of companies. Risk profile is important for the customer of a financial advisor and measured by MIFID today….but these questions don’t say anything about the risk awareness of the investor. We first go through a case study of a couple and the professor explains the different investment categories and the return for each investment category.

The professor goes in detail explaining this case study of a retired couple where you can see 4 scenarios of investments. Real estate is one scenario that can drop in price in the future (example is the 20% drop in Antwerp for apartment prices)

Today there’s nobody that thinks that we can’t pay pensions in the future…what would happen if government cannot pay pensions….governments can not be trusted. See for example in Russia. Today this is not the case in Belgium and is a government pension assured.

Advice: somebody who is strongly invested, needs to be invested in STOCKS according the professor. The government pension of a professor with little real estate is mainly invested in STOCKS.

Living of dividends ? He does not agree and think it is NOT possible with an average return of 5 – 6%. If you have an age of 76 you still need a 30 year investment portfolio.

The professor is mainly invested in S&P500 and EUROSTOXX stocks. He is negative towards the future. A correction can not be predicted but when she comes…it will be a steap decrease. So here are his two tips.

TIP 1 : DO NOT INVEST IN INDEX FUNDS AND ETFs

TIP 2 : GOLD IS AN ATTRACTIVE DIVERSIFIED INVESTMENT

Gold is a strange investment that does not generate any money. Any rational investor does not invest in gold as you just put it away in a suitcase. Average return on gold is 7%. It is although an insurance against the governments and central banks.

You can download the Dutch presentation with below link

Our opinion

The professor is clearly an expert in Financial planning since years and we agree that being invested in the stock market is the best way to grow your wealth if you invest disciplined without emotions, with knowledge and with a clear strategy and objective in mind. Although a pension may be “assured” by the government, it will not be sufficient to pay for a pension home. Read our recent blog post “How you can LOSE all your net worth and make also your kids poorer….ACT NOW !” about this topic as this is a MUST READ ! ![]()

We although don’t agree that living from dividends is not possible. I agree with the professor only if you invest in Belgian dividend stocks… There are plenty of people living off dividends. I won’t list them all but an example is Mr Tako Escapes who lives completely from his dividends. Of course the Belgian government has made it very difficult after increasing their dividend tax to 30%. They now realize that they no longer can milk further the investor and tax income is going down. Let’s hope this tax goes back to a reasonable % as Belgians seem always want to lead the chart in government taxes within Europe.

We don’t believe in the tips of the professor and his reasoning behind ETF investing. I personally believe more the reasoning of professor Lance Brofman, Ph.D. economics and Finance MBA in the USA who is an expert in ETF investing. You can find some articles on Seekingalpha.com. Decide for yourself what is your risk management profile and who you believe.

The professor is a fan of investing in gold. Investing in gold as an asset is not part of our investment strategy. If you invest in gold, you should only invest 5% as this 5% gold (coins or bars) won’t give you any passive income during all the years you hold it in your possession. I rather want to invest my money in other asset categories that can generate a consistent passive income. If you want to invest in gold, you can also invest in the GOLD ETF tracker GLD. This tracker is currently in an uptrend channel with resistance at 122 – 122,5 $ level.

Presentation 2 : Live longer without worries (Ingrid Stevens)

Mrs. Ingrid Stevens is the CEO of a family owned wealth planning company Leo Stevens & Cie. Ingrid has been a student of Prof. Emiel Van Broekhoven and feels honored to present after her professor. This presentation is about important questions we never ask ourselves.

Today there is a clear lack of financial literacy, financial planning in general and all the Belgian laws around it. Important questions about finance and future care need to be asked in life. And this goes over generations. An example of a cheated spouse and the importance of a marriage contract is explained in detail. Mrs. Stevens highlights that she wrote two interesting books about these topics :

When you click above URL links, you can find the website where to order them.

As time evolved, Mrs. Stevens received many succession and heritage planning questions but also many financial care questions. Cancer patients (kids with cancer), parents with dementia, …

These questions were focussed on daily care assurance and financial peace of mind. It would be sad to have a succession or heritage planning where majority of your wealth goes to the government.

There are 4 foundations for a good plan

- Financial planning

- Real Estate planning : fiscal, legal and financial plan

- Insurance coverage : what to do in case of sickness, handicap,…guaranteed income

- Protection of the UNEXPECTED : what in case of dementia, coma, accident, deteriorating health, not possible to execute your company activities,.…

A stroke can hit you also at younger age…so be prepared. Mrs. Stevens highlights and explains the power of attorney for care. (Voorzorgsvolmacht) She explains the content of this contract which you need to submit at a notary. It costs 300 – 400 Euro max.

This contract can be a first step in your heritage planning which is always a difficult topic to discuss. Kids need to discuss…

At the end, Mrs. Stevens pledges for a “spiritual” testimony where you write on ONE PAPER WITH BULLETS….WHAT ARE THE VALUES TO BE PASSED ON TO YOUR FUTURE GENERATIONS ?

This has no legal value but leaves your kids and grandkids with a great memory for what you stand for in life!

Our opinion

This presentation was very insightful and full of very important information. We purchased the two books and read already some chapters that will be applicable in my family. We can definitely recommend you those two books. It can give you the required knowledge for good and bad days.

I personally never had heard about this power of attorney for care. (Voorzorgsvolmacht)

You can download the Dutch presentation with below link and we recommend you to read all slides

2. Ingrid Stevens – Langer leven zonder zorgen

Presentation 3 : Real estate a Cornerstone of your net worth (Thomas Weyts)

Mr. Thomas Weyts works for the company Lemonconsult and starts with stating the fact that 50% of wealth is real estate in Belgium. The sad reality is your future pension. In order to sustain your living standards an average family needs 36.000 Euro. So in order to ensure your capital and wealth, you need to calculate your cash deficits or shortages when you retire. Your pension will NOT be sufficient. Today there are 4 working people for 6 pension payouts…soon it will be 3 working people and in 2060. 2 working people will have to pay all pension payouts….crazy isn’t it? And the government is NOT prepared…

There are 4 pension pilars and in the 4th pilar real estate should be an asset in which you have invested. 7 out of 10 Flemish family own a house. In Brussels it is only 42%. Previous years it was 60%.

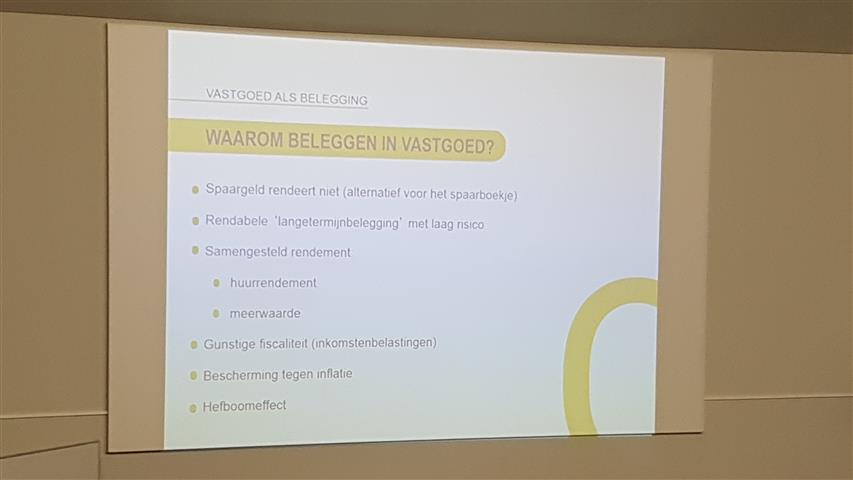

Investing in real estate for rental properties. Mr. Weyts explains all the reasons why this is a wise choice and also describes the involved risks. For every real estate investment you must make a cashflow calculation  . Be conservative with your rental income and add your maintenance fees.

. Be conservative with your rental income and add your maintenance fees.

Why invest in Real estate

It is a good alternative for a savings account. It is a long term investment for 15 years.

Big banks have 170 billion saving money and more money goes today to real estate. Investors want more return on their money by investing in real estate. There can be a gain in the form of rental income.

Rental prices have gone up over time. Your final return can be around 4% with low risk according to Mr. Weyts. He ends with explaining how to pass on real estate to your kids and future generations.

Prof. Van Broekhoven comments at the end that the average return of investing in stocks is : 4,85% – it can be 11% if you are a good investor. For him, the NET return of real estate is 3%.

You have to calculate your NET RETURN. With real estate you don’t know what the future value of your property will be going forward.

Our opinion

This was a very thorough presentation covering all aspects of investing in real estate. While investing in your own house may be a good choice, I believe that current house and apartment prices are driven up solely due to the fact that savings accounts do not return any value. Flemish people have the strong belief that investing in your own house is a MUST and the best insurance for your future pension. This belief is also passed on to the children. We have seen this conclusion during the Big Debate with students. Read here the blogpost The BIG Debate : Things to do with your money and how students think about money. In that debate investing in real estate was not recommended by the panel members.

In our opinion you need a lot of spare time if you want to invest in real estate and the risks outweights the average net return of 3%. An average return of 3% is hardly higher than the inflation of 2,93%. Not worth my time…

You can download the Dutch presentation with below link

3. Thomas Weyts – vastgoed als bouwsteen van uw vermogen

Presentation 4 : Investing in practice – A Personal Total Vision (Jo Stremersch)

Mr. Stremersch runs with his partners a personal financial planning company. He beliefs that you need to start from a total personal vision. Good advice is everywhere today in a world full of robo-advisors, media, blogs, private and wealth bankers….but at the end you are part of someone’ else agenda.

You need to ask yourself as investor the following questions :

- What do I expect for my investment portfolio?

- What are your priorities ?

- Where do you want to “shop”?

His wife says that she will go shopping shoes…and then she returns with 3 dresses. Woman’s logic..

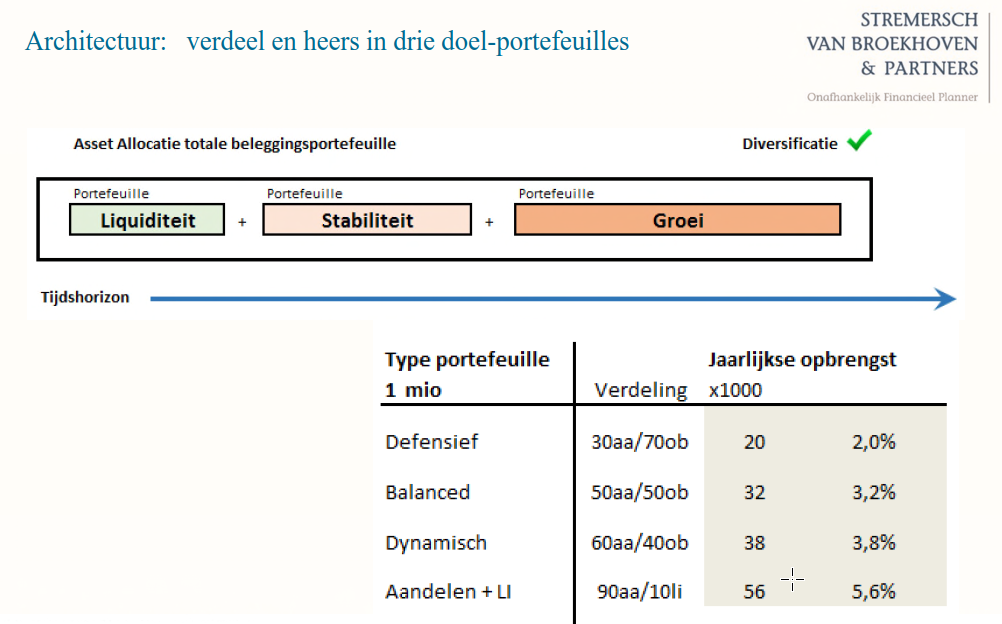

Financial planning consists of two main activities. Nr 1 is building your private office (slide 7) which consists of your real estate, your company, heritage planning,… The second one is your investments where your portfolio requires solid guidance and continuous follow up. Start with making an inventory of your net worth. Then make a cash flow forecast for the next 10 years. A permanent cash flow income stream is not easy. What asset allocations should you chose? What is your potential return per asset allocation? Where can you be in 10, 20, 30 years?

Mr. Stremersch advices to setup three purpose portfolios. One is cash available on a savingsaccount with no return. Portfolio 2 is focussed on stability. Portfolio 3 wants to grow your money. You can estimate the yearly return for each portfolio.

The key question is “Should you outsource your investments portfolio ?”

The average investor does have a poor yearly return because he invests with emotions. He is also playball of the media and investing at the wrong moments. When we review the different asset categories, we can conclude that bonds have increasing risks. This is not a good asset to invest in today. Investing in stocks is the best thing to do today as there really is no alternative (TRINA) Although you need to spread in time, countries and sectors and focus on solid international companies with clear cashflow and stable dividend payouts.

How does Stremersch, Van Broekhoven Partners execute portfolio management?

First they do an inventory of the current portfolio. Is the current portfolio managed cost efficient? Most portfolios have high costs because they consist of high cost mutual funds. (slide 24) The return of the end customer is very low or even negative. Common conclusions after reviewing portfolios can be summarized as following overview.

Step 2 of his company approach is to write out a RFI/RFP and create a strategy to build a new portfolio with an expected return on investment. You will need to transfer ownership with clear conditions. The total structure of your portfolio will be composed for example of three pilars. One with a focus on growth countries, one part focussed on EU and US stocks and one part composed of trackers and funds. Step 3 is the final contract with clear expectations and monitoring of your portfolio.

The final goal of this whole approach and outsourcing your portfolio is PEACE of MIND.

Our opinion

From this presentation we remember two important key learnings. Number 1 is create a cash flow forecast for the next 5 – 10 – 20 years. As described in our Financial strategy, we focus on cash flow streams and making such an cash flow overview is quite interesting and important (see slide 9). Our second key learning was the investment approach of an independent financial planner and how he applies diversification. Normally spreading your investments is equal to suffering. Why? Most financial advisors recommend you to spread your investments in bonds, stocks, gold and real estate. This is done with the objective to lower your risk. But diversification results often in a lower return. What most unexperienced and unknowledgeable investors don’t know is that private banks and financial advisors don’t want to pursue maximum return but only want to put your wealth under their monitoring and management. They earn money while you carry the risk. In an increasing or decreasing stock market they charge fees, even when you have a loss.

There is definitely a market for financial advisors that can assist wealthy customers with little to no time or knowledge of investing in the stock market. But as an investor you should know that you pay a price for this service, knowledge with no guarantee on a better return on investment. At a VFB conference I once encountered an investor who had outsourced his 350k portfolio and his return per year was negative. Now he was investing in his knowledge to become a Do IT YOURSELF (DIY) investor. Mr. Stremersch mentioned that good advice is everywhere and when looking at competitive services (robo advisors, blogs, private bankers,..), you fit in someone else’s agenda. In a sense when you outsource your portfolio to a financial planner company, you as an investor become part of his’ company agenda….right? It was definitely interesting to learn the strategy of an independent financial planner.

Our advice is Keep it simple. Some people like complex solutions and think they need to outsource to banks, financial planners, robo advisors,… Those companies know that most of you haven’t invested in your financial knowledge and with throwing some complex jargon to you, they are regarded as the investment experts. Actually investing in the stock market is not that difficult, but therefor not easy. You just need to focus on three d’s (as I read in a recent article) : Discipline, Diversification with a focus on return, and Dividend. If you know nothing about investing, read the following blog post

You know NOTHING about investing money if …..

If you want to read another interesting article about financial planners or advisors, read the following article “4 Signs That Your Financial Advisor is Ripping you off”

You can download the Dutch presentation with below link

4. Jo Stremersch – Doelgericht beleggen

Final conclusion

While driving home, we reflected on this interesting VFB event full of investment advice. Our key learnings are described above and our next actions are focused on the points highlighted in the presentation of Mrs. Stevens. This presentation was the most interesting of this VFB event.

Our primary action going forward will be to put a power of attorney for care (voorzorgsvolmacht) in place for the care of my mom. We purchased the books and started to read the most important financial life questions within the books. We definitely encourage you to ask yourself the same important life questions about finance and care. Questions we all want to delay as much as possible…

Special thanks to VFB for setting up this event. When we increase our financial knowledge, we are happy ! We end with a final quote to make you think…

Good luck with your financial strategy? Did you learn something from this blogpost? What is your opinion? Don’t hesitate to leave your comments and feedback…

Follow my blog with Bloglovin

3 Response Comments

What’s your take on index trackers? I totally get the lessons, but for me 2 3 index trackers seem like a simple way to get in the diversified stock market. Will definitely read more about that “voorzorgsvolmacht”.

Yes index trackers are also a way to diversify your investments. I read in a lot of blogs that people invest in index funds. The most popular one is Mr Money Mustache (www.mrmoneymustache.com)

Just be aware when to step out of the market. But most importantly spread your investments with a continuous monthly amount so you also buy at the dips of the market.

We do not invest in index funds (for now) as the dividend % is low for those index trackers and we focus on passive income. Maybe we will do in the future.

Thanks for the feedback and question !

thx for the write up. A lot to read and think about. I think I will start to look i to the other aspects as well, like the zorgvolmact.

I do invest in trackers, accumulating ones. I do not need the dividend now and this is a tax efficient way to be invested.