Hello again. Here’s the dividend income report of March 2017 for my kids’ portfolio!

After their trip to Paris, my kids went back to school with enthusiasm to tell all their friends about their adventures in Paris. It was definitely a great City break trip. If you missed the blog post, you can read our daily program here. It was a great learning experience for them and you can admire a lot of nice pictures in our blogpost. In March there was a pyjama day at my daughter’s school (going to school in cold march in a pyama…how crazy can it get?) and my son enjoyed some movies. He is a movie fanatic and also loves to read books. At the end of March kids had great school results. So…nothing to complain about ! And April is already progressing fast…time flies !

Now you can read our Dividend Income March 2017 Report Out

Dividends received in March 2017

During the month of March 2017, we received 59,23$ dividend income. The first dividend came from a small investment in an European company. This company paid us 35,94 Euro. This is a yearly dividend (typical for European companies) The other dividend payout was 20,82 $ from a monthly paying stock. We used the currency exchange rate of 31st March to convert the 35,94 Euro into 38,41 dollar.

![]()

Another good month and we keep on grinding further… building that cash flow in our portfolio.

Portfolio analysis and Growth

During the month of March, we also optimized our kids portfolio.

We also owned the company WHLR in my kids portfolio. This stock paid nicely for two months. As described and explained in my March 2017 my Own Portfolio Dividend Income Report, we said goodbye to Wheeler and we increased our position in a high paying ETF that pays us on a quarterly basis 14%.

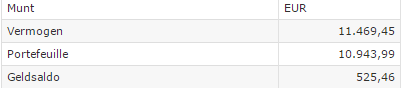

Our cash position has been reduced to approximately 500 Euro. Here you can see a screenshot of the value of our kids portfolio.

We now have 126,78 dollar + 35,94 euro dividends received on a starting amount of 10.000 EURO AFTER JUST 3 MONTHS.

The 2017 goal for my kids’ portfolio is to generate 600$ in the total year which equals to an investment return of 6%. A good return on investment I would say compared to the alternatives. We now have 27% of our 2017 Yearly goal on our bankaccount. This is what matters…money paid on our bank account.

CASH FLOW and Dividend Income, that is our only focus !

Going forward

We don’t have any goals for our kids portfolio. Just watching our dividends coming into our bank account and building enough cash to make another investment. And that is all what counts and gives us pleasure !! With the new investments made in march, it will be interesting to see what the impact will be in april for our cash flow.

Good luck with your personal finance strategy for your kids! Putting money on a savings account for your kids is NOT a strategy to make it grow!

8 Response Comments

I completely agree. We have to be more active with our investments than just letting the banks hold the money. Need to be proactive.

That is great having a dividend portfolio for your kids. I have 2 amazing sons now, and I was thinking of starting one for each of them. I have not decided the best way to that way. Maybe it is time I do.

Congrats with your 2 amazing sons. I am sure they give you a lot of joy.

The sooner you start a portfolio, the faster the snowball effect. The size of the portfolio doesn’t matter so much. We invested first years with a fund investment plan and doubled our money in 6 years time. I mainly think I got lucky on my timing and with consistent monthly investments, the snowball effect got bigger rapidly. The 10K is now converted in a dividend portfolio which I can manage more actively. Within a fund plan of the bank you can only arbitrage your different fund allocations with a penalty also as result.

It all depends how you want to manage it or not. A savings account is definitely not a strategy to pursue.

Good luck with growing your kids’ money !

Since I actively manage my account, I do not know if I want to actively manage 2 more accounts. I may just use some good dividend ETF’s for them and actively stock pick in mine. Maybe I should open the accounts and get the money in their, and then worry about picking something. Thank you for the input.

Agreed, a savings account for kids is not a good solution. It is a guarantee to loose money to inflation.

We have a monthly investment plan in place. I can not wait for some robo advisor to attack the BE market with small amounts.

Prittle already does that, I just do not feel happy with the high nr of ETF they have.

For the money they get from family or grand parents, we also have a KEY PLAN in place. We add 25 Euro per month to that. The 10k portfolio was a previous keyplan in which we no longer put money. This one has to grow by dividend cash flow and capital gains.

ETF matic is another Robo-adviser that recently launched. I just don’t like the fees. I still prefer to make the decisions myself :-))

Awesome update. I love reading about parents who open an investment account for their kids. Just keep building that passive income stream bit by bit and take advantage of all the time young people have. No savings accounts here. Just diversified stocks paying solid dividends.

You are so smart to introduce investing to your children at such a young age. It will really help them understand the value of money and what compounding interest can accomplish. My parents helped open a custodial account for me when I turned 13. In fact, that is the very same account that I have now (though it has been under my control is about age 18).

Scott